Average Health Insurance Cost? [2024 Guide]

Navigating the world of health insurance can feel like traversing a complex maze. With countless plans, varying coverage levels, and a language all its own, it's easy to feel overwhelmed. Understanding the costs associated with health insurance is a critical first step in making informed decisions about your healthcare. It's not just about finding the cheapest plan; it's about finding the plan that offers the best value for your individual needs and circumstances. This means considering factors like your health history, your tolerance for risk, and the specific services you anticipate needing in the coming year. Choosing a health insurance plan is a significant financial commitment. It impacts your monthly budget and your overall financial security. A well-chosen plan can provide peace of mind, knowing that you're protected against unexpected medical expenses. A poorly chosen plan can lead to financial strain and limited access to care. Therefore, taking the time to understand the intricacies of health insurance costs is an investment in your well-being. Many factors influence the price you pay for health insurance. These include your age, location, the type of plan you choose, and the level of coverage you select. Understanding how these factors interact can help you make more informed decisions. For example, a younger individual might opt for a higher deductible plan with lower monthly premiums, while an older individual might prioritize a plan with lower deductibles and copays, even if it means paying more each month. Moreover, the healthcare landscape is constantly evolving. New regulations, technological advancements, and shifting market dynamics all impact the cost of health insurance. Staying informed about these changes is crucial for making the most of your healthcare dollars. What worked last year might not be the best option this year. So, how much can you expect to pay for health insurance in 2024? To put it simply, the answer varies greatly depending on individual circumstances and plan choices. Let’s delve into the details and explore what influences the **Average Health Insurance Cost? [2024 Guide]**. This exploration will provide a clearer picture of what you can expect to pay for health insurance coverage.

Understanding the Basics of Health Insurance Costs

Premiums: Your Monthly Investment

The premium is the monthly payment you make to your insurance company to maintain your coverage. Think of it as the price you pay to keep your policy active. Premiums are influenced by a variety of factors, including your age, location, the type of plan you choose (e.g., HMO, PPO), and the level of coverage.

Generally, plans with lower deductibles and copays will have higher premiums, while plans with higher deductibles and copays will have lower premiums. This is because you're essentially shifting more of the financial risk to the insurance company in exchange for a higher monthly payment.

Premiums can also be affected by subsidies, which are financial assistance programs that help individuals and families afford health insurance. Subsidies are typically based on income and household size.

Comparing premiums across different plans is a crucial step in choosing the right coverage. However, it's important to consider the overall value of the plan, including deductibles, copays, and the network of providers.

Don't automatically assume that the cheapest plan is the best option. Take the time to carefully evaluate all the costs and benefits before making a decision. A slightly higher premium might be worth it if it means lower out-of-pocket expenses when you need medical care.

Deductibles: Your Out-of-Pocket Responsibility

The deductible is the amount you must pay out of pocket for covered healthcare services before your insurance company starts to pay. For example, if your deductible is $2,000, you'll need to pay the first $2,000 of your medical expenses before your insurance begins to cover the rest.

Deductibles can range from a few hundred dollars to several thousand dollars, depending on the plan you choose. Plans with lower deductibles typically have higher premiums, while plans with higher deductibles have lower premiums.

It's important to choose a deductible that you can realistically afford to pay. If you have a high deductible plan, make sure you have enough savings to cover your deductible in case of an unexpected medical event.

Some plans offer "preventive care" services that are covered even before you meet your deductible. This includes annual checkups, vaccinations, and certain screenings.

Consider your healthcare needs when choosing a deductible. If you anticipate needing frequent medical care, a lower deductible plan might be a better option. If you're generally healthy and don't expect to need much medical care, a higher deductible plan might be more cost-effective.

Copays and Coinsurance: Sharing the Cost

A copay is a fixed amount you pay for a covered healthcare service, such as a doctor's visit or prescription. For example, you might pay a $20 copay to see your primary care physician or a $5 copay for a generic prescription.

Coinsurance is the percentage of the cost of a covered healthcare service that you pay after you've met your deductible. For example, if your coinsurance is 20%, you'll pay 20% of the cost of the service, and your insurance company will pay the remaining 80%.

Copays and coinsurance are designed to share the cost of healthcare between you and your insurance company. They help keep premiums affordable and prevent overuse of medical services.

The specific copays and coinsurance amounts will vary depending on the plan you choose. Some plans might have low copays for certain services but higher coinsurance for others.

Pay attention to the copays and coinsurance amounts when comparing different plans. They can have a significant impact on your out-of-pocket costs, especially if you need frequent medical care.

Out-of-Pocket Maximum: Your Financial Safety Net

The out-of-pocket maximum is the most you'll have to pay for covered healthcare services in a year. Once you reach your out-of-pocket maximum, your insurance company will pay 100% of your covered medical expenses for the rest of the year.

The out-of-pocket maximum includes your deductible, copays, and coinsurance. It does not include your premiums.

The out-of-pocket maximum provides a financial safety net in case you have a serious illness or injury. It protects you from potentially catastrophic medical expenses.

The out-of-pocket maximum varies depending on the plan you choose. Plans with lower premiums typically have higher out-of-pocket maximums, while plans with higher premiums have lower out-of-pocket maximums.

Consider your risk tolerance when choosing an out-of-pocket maximum. If you're risk-averse, you might prefer a plan with a lower out-of-pocket maximum, even if it means paying a higher premium. If you're comfortable with more risk, you might opt for a plan with a higher out-of-pocket maximum and lower premiums.

Factors Influencing Average Health Insurance Cost? [2024 Guide]

Age: A Key Determinant

Age is a significant factor in determining health insurance costs. Older individuals generally require more medical care than younger individuals, so insurance companies typically charge them higher premiums.

This is because older individuals are more likely to develop chronic conditions, such as heart disease, diabetes, and arthritis. They also tend to need more frequent doctor's visits and hospitalizations.

Under the Affordable Care Act (ACA), insurance companies are allowed to charge older individuals up to three times more than younger individuals.

However, age is not the only factor that influences health insurance costs. Other factors, such as location, plan type, and coverage level, also play a role.

It's important to compare different plans and consider your individual healthcare needs when choosing health insurance, regardless of your age.

Location: Where You Live Matters

The cost of health insurance can vary significantly depending on where you live. This is because healthcare costs vary from region to region.

Factors such as the cost of living, the availability of healthcare providers, and the prevalence of certain health conditions can all influence healthcare costs in a particular area.

States with higher healthcare costs tend to have higher health insurance premiums. States with lower healthcare costs tend to have lower health insurance premiums.

Even within a single state, health insurance costs can vary from county to county or even zip code to zip code.

When shopping for health insurance, it's important to compare plans that are available in your specific location. Don't assume that a plan that's affordable in one area will be affordable in another.

Plan Type: HMO, PPO, and More

The type of health insurance plan you choose can also affect your costs. The most common types of plans are HMOs, PPOs, and EPOs.

HMOs (Health Maintenance Organizations) typically have lower premiums than PPOs, but they also have more restrictions. With an HMO, you'll typically need to choose a primary care physician (PCP) who will coordinate your care. You'll also need a referral from your PCP to see a specialist.

PPOs (Preferred Provider Organizations) offer more flexibility than HMOs. With a PPO, you can see any doctor or specialist you want without a referral. However, you'll typically pay more for out-of-network care.

EPOs (Exclusive Provider Organizations) are similar to HMOs in that you'll typically need to stay within the plan's network to receive coverage. However, EPOs typically don't require you to choose a PCP or get referrals to see specialists.

The best type of plan for you will depend on your individual healthcare needs and preferences. If you want the lowest possible premiums and are willing to accept more restrictions, an HMO might be a good choice. If you value flexibility and are willing to pay more, a PPO might be a better option.

Coverage Level: Bronze, Silver, Gold, and Platinum

The level of coverage you choose will also impact your health insurance costs. Plans are typically categorized as Bronze, Silver, Gold, or Platinum, based on the percentage of healthcare costs they cover.

Bronze plans have the lowest premiums but the highest out-of-pocket costs. They typically cover about 60% of healthcare costs, while you pay the remaining 40%.

Silver plans have moderate premiums and moderate out-of-pocket costs. They typically cover about 70% of healthcare costs, while you pay the remaining 30%.

Gold plans have higher premiums but lower out-of-pocket costs. They typically cover about 80% of healthcare costs, while you pay the remaining 20%.

Platinum plans have the highest premiums but the lowest out-of-pocket costs. They typically cover about 90% of healthcare costs, while you pay the remaining 10%.

The best level of coverage for you will depend on your healthcare needs and budget. If you're generally healthy and don't expect to need much medical care, a Bronze or Silver plan might be a good choice. If you have a chronic condition or anticipate needing frequent medical care, a Gold or Platinum plan might be a better option.

The Impact of Subsidies and Tax Credits

Understanding Premium Tax Credits

Premium tax credits are a type of financial assistance that can help lower your monthly health insurance premiums. These credits are available to individuals and families who meet certain income requirements.

The amount of the premium tax credit you receive is based on your income, household size, and the cost of a benchmark health insurance plan in your area.

You can apply for premium tax credits when you enroll in health insurance through the Health Insurance Marketplace (also known as the Exchange).

If you're eligible for a premium tax credit, you can choose to have it paid directly to your insurance company, which will lower your monthly premium. Alternatively, you can choose to claim the credit when you file your taxes.

Premium tax credits can make health insurance much more affordable for many people. If you're struggling to afford health insurance, it's worth checking to see if you're eligible for a premium tax credit.

Cost-Sharing Reductions: Lowering Out-of-Pocket Expenses

Cost-sharing reductions are another type of financial assistance that can help lower your out-of-pocket healthcare costs. These reductions are available to individuals and families who meet certain income requirements and enroll in a Silver plan through the Health Insurance Marketplace.

Cost-sharing reductions lower the amount you have to pay for deductibles, copays, and coinsurance.

The amount of the cost-sharing reduction you receive is based on your income and household size.

If you're eligible for cost-sharing reductions, you'll automatically receive them when you enroll in a Silver plan through the Health Insurance Marketplace.

Cost-sharing reductions can significantly lower your out-of-pocket healthcare costs, making it easier to afford the care you need.

Eligibility Requirements for Subsidies

To be eligible for premium tax credits and cost-sharing reductions, you must meet certain income requirements. These requirements vary depending on your household size and the state in which you live.

Generally, you're eligible for premium tax credits if your household income is between 100% and 400% of the federal poverty level.

You're eligible for cost-sharing reductions if your household income is between 100% and 250% of the federal poverty level.

You must also meet other requirements, such as being a U.S. citizen or legal resident and not being eligible for other forms of health insurance, such as Medicare or Medicaid.

You can use the Health Insurance Marketplace's website to determine if you're eligible for subsidies. The website has a tool that can estimate your eligibility based on your income and household size.

How to Apply for Subsidies

To apply for premium tax credits and cost-sharing reductions, you must enroll in health insurance through the Health Insurance Marketplace. The Marketplace is an online platform where you can compare different health insurance plans and apply for subsidies.

You can enroll in health insurance through the Marketplace during the annual open enrollment period, which typically runs from November 1 to January 15. You may also be able to enroll outside of the open enrollment period if you experience a qualifying life event, such as losing your job or getting married.

When you apply for health insurance through the Marketplace, you'll need to provide information about your income, household size, and other relevant details.

The Marketplace will use this information to determine if you're eligible for subsidies and to calculate the amount of your subsidies.

Once you've enrolled in a health insurance plan through the Marketplace, your subsidies will be applied to your monthly premiums or your out-of-pocket healthcare costs.

Employer-Sponsored Health Insurance vs. Individual Plans

The Benefits of Employer-Sponsored Plans

Employer-sponsored health insurance plans are often more affordable than individual health insurance plans because employers typically pay a portion of the premiums.

Employer-sponsored plans also tend to offer a wider range of coverage options than individual plans.

Another advantage of employer-sponsored plans is that they're often easier to understand and manage. Your employer's human resources department can help you navigate the plan and answer any questions you have.

However, employer-sponsored plans may not be the best option for everyone. If you have specific healthcare needs or preferences, you may be better off with an individual plan that you can customize to your specific requirements.

Ultimately, the best type of health insurance plan for you will depend on your individual circumstances.

Understanding Individual Health Insurance Options

Individual health insurance plans are purchased directly from an insurance company or through the Health Insurance Marketplace. These plans are typically more expensive than employer-sponsored plans, but they offer more flexibility and customization.

With an individual plan, you can choose the specific level of coverage you need and select a plan that fits your budget.

Individual plans are a good option for people who are self-employed, unemployed, or who don't have access to employer-sponsored health insurance.

However, individual plans can be more complex to navigate than employer-sponsored plans. You'll need to do your research to find a plan that meets your needs and understand the terms and conditions of the policy.

It's also important to note that individual plans are subject to open enrollment periods, so you'll need to enroll during the designated time frame to avoid a gap in coverage.

Comparing Costs and Coverage

When comparing employer-sponsored and individual health insurance plans, it's important to consider both the costs and the coverage.

Compare the monthly premiums, deductibles, copays, and coinsurance amounts for each plan. Also, review the plan's covered services and any limitations or exclusions.

Consider your healthcare needs and preferences when making your decision. If you have specific medical conditions or require frequent medical care, you'll want to choose a plan that offers comprehensive coverage.

If you're generally healthy and don't anticipate needing much medical care, you may be able to save money by choosing a plan with lower premiums and higher out-of-pocket costs.

Ultimately, the best way to compare health insurance plans is to create a spreadsheet that outlines the costs and coverage for each option. This will help you make an informed decision and choose the plan that's right for you.

The Role of the Health Insurance Marketplace

The Health Insurance Marketplace is an online platform where you can compare different individual health insurance plans and apply for subsidies. The Marketplace was created under the Affordable Care Act (ACA) to make it easier for people to find and afford health insurance.

The Marketplace allows you to compare plans based on price, coverage, and other factors. You can also use the Marketplace to estimate your eligibility for premium tax credits and cost-sharing reductions.

The Marketplace is a valuable resource for anyone who is looking for individual health insurance. It can help you find a plan that meets your needs and fits your budget.

To use the Marketplace, you'll need to create an account and provide information about your income, household size, and other relevant details.

Once you've created an account, you can browse the available plans and compare their costs and coverage. You can also use the Marketplace to apply for subsidies and enroll in a plan.

Tips for Lowering Your Health Insurance Costs

Increasing Your Deductible

One way to lower your health insurance premiums is to increase your deductible. A deductible is the amount you have to pay out of pocket for covered healthcare services before your insurance company starts to pay.

Plans with higher deductibles typically have lower premiums, while plans with lower deductibles have higher premiums.

If you're generally healthy and don't expect to need much medical care, increasing your deductible can be a good way to save money on your health insurance premiums.

However, it's important to make sure you can afford to pay your deductible if you do need medical care. If you have a high deductible plan, you'll need to have enough savings to cover your deductible in case of an emergency.

Before increasing your deductible, consider your healthcare needs and your budget. If you anticipate needing frequent medical care, a lower deductible plan might be a better option.

Choosing a Different Plan Type

Another way to lower your health insurance costs is to choose a different plan type. As mentioned earlier, HMOs typically have lower premiums than PPOs, but they also have more restrictions.

If you're willing to accept more restrictions in exchange for lower premiums, an HMO might be a good choice for you.

However, it's important to make sure that the HMO's network includes the doctors and hospitals you want to see. If you prefer to have more flexibility in choosing your healthcare providers, a PPO might be a better option.

Consider your healthcare needs and preferences when choosing a plan type. If you value flexibility and are willing to pay more, a PPO might be the best choice. If you're looking for the lowest possible premiums and are willing to accept more restrictions, an HMO might be a better option.

EPOs offer a middle ground. They often have lower premiums than PPOs while still providing access to a broad network of providers, although out-of-network care is generally not covered.

Negotiating Medical Bills

Did you know that you can often negotiate your medical bills? Many hospitals and doctors are willing to negotiate the price of their services, especially if you pay in cash or if you're uninsured.

Don't be afraid to ask for a discount. You can also ask for an itemized bill and review it carefully for any errors or duplicate charges.

If you're struggling to pay your medical bills, you can also ask the hospital or doctor about payment plans or financial assistance programs.

Negotiating your medical bills can save you a significant amount of money, so it's always worth a try.

Some organizations specialize in helping patients negotiate medical bills. Consider seeking their assistance if you feel overwhelmed or unsure of where to begin.

Taking Advantage of Preventive Care

Most health insurance plans cover preventive care services, such as annual checkups, vaccinations, and certain screenings, without requiring you to pay a deductible or copay.

Taking advantage of preventive care services can help you stay healthy and prevent serious illnesses from developing. This can save you money on healthcare costs in the long run.

Talk to your doctor about what preventive care services are right for you. Make sure to schedule regular checkups and screenings to stay on top of your health.

Preventive care is not only good for your health, but it's also good for your wallet.

Many insurance plans also offer incentives for participating in wellness programs, such as gym memberships or smoking cessation programs. These programs can help you improve your health and lower your healthcare costs.

Average Health Insurance Cost? [2024 Guide]: What to Expect

National Averages for Different Plan Types

It's important to note that the **Average Health Insurance Cost? [2024 Guide]** varies considerably based on several factors, as we have discussed. However, understanding national averages can provide a benchmark as you begin your research.

Generally, employer-sponsored health insurance tends to be more affordable than individual plans due to the employer's contribution.

Individual health insurance costs vary widely based on the metal tier (Bronze, Silver, Gold, Platinum), with Bronze plans having the lowest premiums and Platinum plans the highest.

HMO plans tend to have lower premiums than PPO plans, but they also offer less flexibility in terms of provider choice.

It's crucial to compare plans carefully, considering not just the premium but also the deductible, copays, coinsurance, and out-of-pocket maximum.

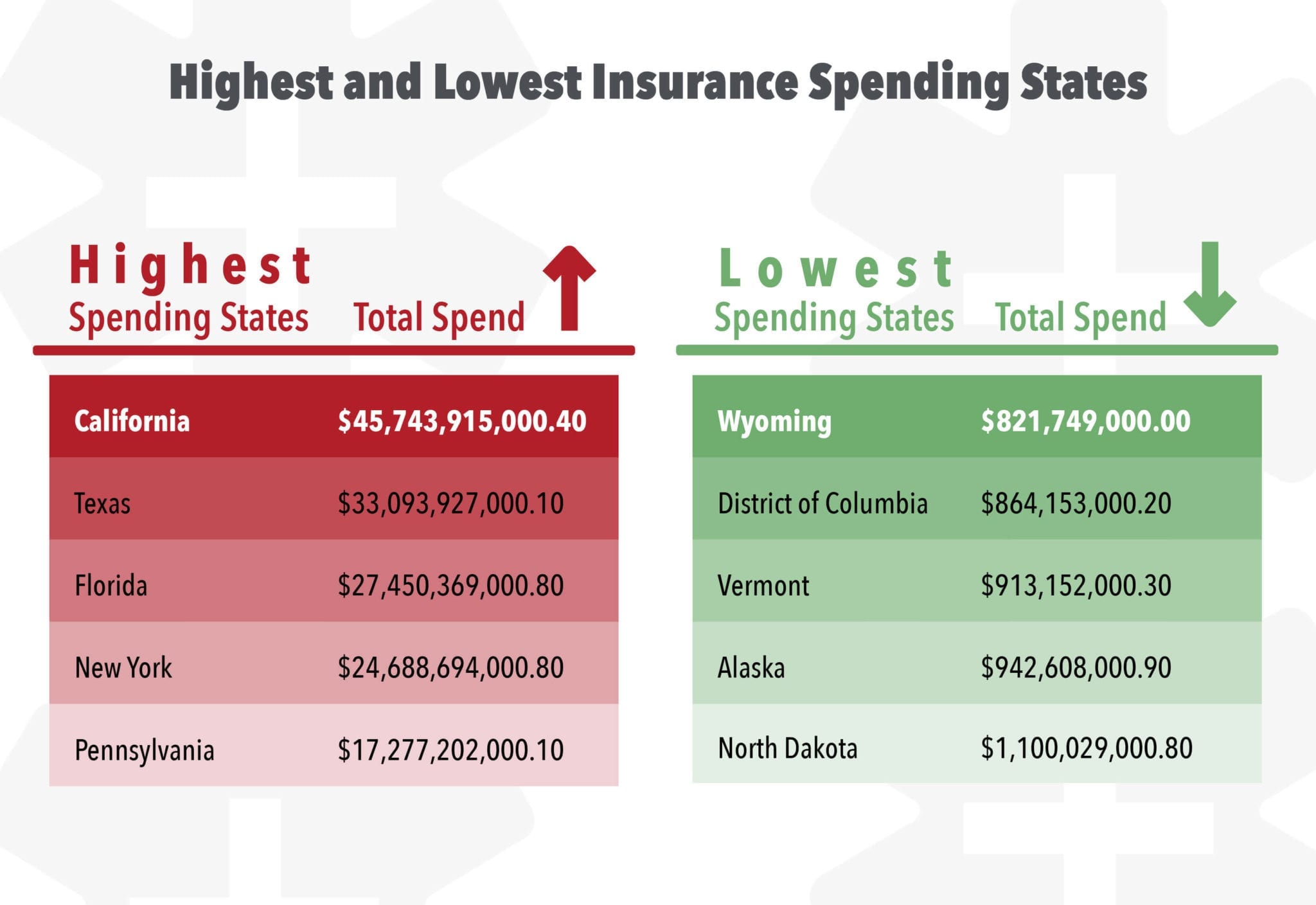

State-Specific Cost Variations

As mentioned earlier, location plays a significant role in determining health insurance costs. Some states have higher healthcare costs than others, which translates to higher premiums.

Factors such as the cost of living, the prevalence of certain health conditions, and the availability of healthcare providers can all influence health insurance costs in a particular state.

States with robust state-level exchanges and strong consumer protections tend to have more affordable health insurance options.

It's important to research the specific health insurance market in your state to get an accurate picture of the costs and coverage options available to you.

Consider consulting with a local insurance agent or broker who can provide personalized guidance and help you navigate the complexities of your state's health insurance market.

The Impact of the Affordable Care Act (ACA)

The Affordable Care Act (ACA) has significantly impacted the health insurance landscape in the United States. The ACA has expanded access to health insurance, provided subsidies to help people afford coverage, and established minimum standards for health insurance plans.

The ACA has also eliminated pre-existing condition exclusions, ensuring that people with pre-existing health conditions can get health insurance.

However, the ACA has also faced challenges, and some of its provisions have been modified or repealed.

The future of the ACA remains uncertain, and any changes to the law could have a significant impact on health insurance costs and coverage options.

Staying informed about the ACA and any proposed changes is crucial for making informed decisions about your health insurance.

Planning Your Budget for Health Insurance

When planning your budget, it's important to factor in the costs of health insurance. This includes your monthly premiums, as well as any out-of-pocket expenses you might incur, such as deductibles, copays, and coinsurance.

Consider setting aside a portion of your income each month to cover your health insurance costs. You can also explore options for lowering your costs, such as increasing your deductible or choosing a different plan type.

Remember that health insurance is an investment in your health and well-being. Don't skimp on coverage to save money, as this could end up costing you more in the long run.

Prioritize your health and budget accordingly. A well-chosen health insurance plan can provide peace of mind and protect you from unexpected medical expenses.

Tools and resources are available online to help you estimate your health insurance costs and plan your budget. Take advantage of these resources to make informed decisions.

Conclusion

Understanding the **Average Health Insurance Cost? [2024 Guide]** is a multifaceted endeavor, impacted by factors ranging from your personal demographics to the broader healthcare landscape. While averages provide a helpful starting point, your specific cost will be determined by your individual circumstances and choices. Take the time to carefully consider your needs, explore your options, and seek professional guidance if needed. Armed with knowledge, you can make informed decisions that protect your health and your financial well-being.

Remember to compare plans, consider subsidies, and explore cost-saving strategies. Health insurance is a complex but essential aspect of personal finance. Stay informed, stay proactive, and stay healthy.

We hope this guide has been helpful in shedding light on the intricacies of health insurance costs in 2024. Remember, navigating the healthcare system can be challenging, but with the right knowledge and resources, you can make informed decisions that are right for you and your family.

Check out our other articles for more in-depth information on related topics, such as choosing the right health insurance plan, understanding your healthcare rights, and navigating the healthcare system. Knowledge is power, and we're here to empower you with the information you need to make informed decisions about your health and your finances.

We are committed to providing you with accurate and up-to-date information to help you navigate the complexities of the healthcare system. Stay tuned for more articles, guides, and resources to help you make the most of your healthcare coverage.

- The average cost of health insurance in the US is about $540 per month