Health Insurance Cost Per Month: What To Expect?

Navigating the world of health insurance can feel like trying to decipher a secret code. Jargon like "deductibles," "copays," and "coinsurance" swirl around, often obscuring the most fundamental question: how much will this actually cost me each month? It's a question that weighs heavily on the minds of individuals, families, and small business owners alike. The price of healthcare has been steadily rising, making health insurance a significant line item in most budgets.

Understanding the landscape of health insurance options is crucial before even considering the monthly premiums. Factors like your age, location, health status, and the type of coverage you choose will all play a role in determining your monthly costs. It's not simply a one-size-fits-all situation; rather, it's a personalized puzzle with multiple variables.

Many find themselves overwhelmed by the sheer volume of choices available. Should you opt for a high-deductible plan with a lower monthly premium, or a more comprehensive plan that offers better coverage but comes with a steeper price tag? What about government subsidies or tax credits – are you eligible, and how do they impact your overall cost?

Furthermore, the specific needs of your family need to be considered. Do you have children who require regular doctor visits? Are there any pre-existing conditions that demand specialized care? These factors will significantly influence the type of plan that's right for you, and consequently, how much you'll be paying each month.

Therefore, it's essential to arm yourself with knowledge and resources to make informed decisions. This guide aims to demystify the process and provide you with a clearer understanding of what to expect when it comes to your **Health Insurance Cost Per Month: What to Expect?** We'll explore the different factors that influence premiums, the various types of plans available, and strategies for finding the most affordable coverage that meets your individual needs.

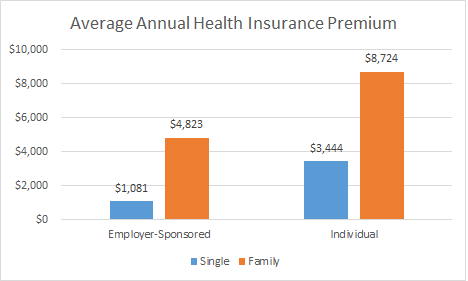

The price you pay for health insurance each month isn't pulled out of thin air. It's a calculated figure based on a variety of factors that insurers use to assess risk. Understanding these factors is the first step in understanding how your monthly premium is determined. Age is a primary factor in determining health insurance costs. Generally, older individuals are statistically more likely to require medical care, so insurance companies often charge them higher premiums. This is based on the principle of risk assessment – the greater the perceived risk, the higher the cost. Younger individuals, on the other hand, typically enjoy lower premiums because they are statistically less likely to require extensive medical treatment. However, this doesn't mean that young people should forgo health insurance. Unexpected illnesses and injuries can strike at any age, making coverage essential. The age-related increase in premiums isn't linear. It tends to become more pronounced as individuals enter their 50s and 60s. This is because the likelihood of developing age-related health conditions increases significantly during these years. It's important to note that the impact of age on premiums can vary depending on the specific insurance plan and the state in which you reside. Some states have regulations that limit the amount by which insurers can increase premiums based on age. Regardless of your age, it's crucial to shop around and compare quotes from multiple insurers to find the most affordable coverage that meets your needs. Don't assume that the first quote you receive is the best one. Your geographical location plays a significant role in determining your health insurance costs. Healthcare costs vary dramatically from one region to another, and these variations are reflected in insurance premiums. Areas with a higher cost of living, a greater concentration of specialists, or a higher utilization of medical services tend to have higher premiums. This is because insurers need to cover the increased costs of providing healthcare in these regions. Rural areas may also experience higher premiums due to a limited number of healthcare providers and a lack of competition among insurers. This can result in higher prices for consumers. State regulations also play a role in determining premiums. Some states have implemented regulations that limit the amount by which insurers can increase premiums, while others have more lenient regulations. To get a clear picture of how your location affects your health insurance costs, it's essential to compare quotes from insurers that operate in your specific area. Online tools and resources can help you quickly compare plans and prices. Your health status, including any pre-existing conditions, can influence your health insurance premiums. While the Affordable Care Act (ACA) prohibits insurers from denying coverage or charging higher premiums based solely on pre-existing conditions, your overall health can still impact your rates. For example, individuals with chronic conditions like diabetes or heart disease may require more frequent medical care, which can translate into higher premiums. Insurers take these factors into account when assessing risk. Lifestyle factors, such as smoking and obesity, can also impact premiums. Some insurers may charge higher rates to individuals who engage in these behaviors, as they are associated with increased health risks. It's important to be honest and transparent about your health status when applying for health insurance. Concealing information can lead to denial of coverage or cancellation of your policy. If you have a pre-existing condition, it's crucial to explore all available options, including plans offered through the ACA marketplace. These plans are guaranteed to cover pre-existing conditions without charging discriminatory premiums. The type of health insurance plan you choose will significantly impact your monthly premium. Different plan types offer varying levels of coverage and flexibility, and these differences are reflected in the cost. Health Maintenance Organizations (HMOs) typically have lower premiums but require you to choose a primary care physician (PCP) who coordinates your care. You'll generally need a referral from your PCP to see a specialist. Preferred Provider Organizations (PPOs) offer more flexibility than HMOs. You can see any doctor or specialist without a referral, but you'll pay less if you stay within the plan's network of providers. Exclusive Provider Organizations (EPOs) are similar to PPOs, but you're generally only covered if you see providers within the plan's network. There's typically no out-of-network coverage, except in emergencies. High-Deductible Health Plans (HDHPs) have lower premiums but higher deductibles. This means you'll pay more out-of-pocket before your insurance coverage kicks in. HDHPs are often paired with a Health Savings Account (HSA), which allows you to save money tax-free for healthcare expenses. When choosing a plan type, consider your individual healthcare needs and preferences. If you value flexibility and the ability to see any doctor without a referral, a PPO may be the best choice. If you're looking for the lowest possible premium and don't mind coordinating your care through a PCP, an HMO may be a better option. The Affordable Care Act (ACA) categorizes health insurance plans into four metal levels: Bronze, Silver, Gold, and Platinum. These levels represent the percentage of healthcare costs that the plan is expected to cover, on average. Bronze plans have the lowest premiums but the highest out-of-pocket costs. They typically cover 60% of healthcare costs, with the remaining 40% being the responsibility of the insured. Silver plans have moderate premiums and moderate out-of-pocket costs. They typically cover 70% of healthcare costs, with the remaining 30% being the responsibility of the insured. Gold plans have higher premiums but lower out-of-pocket costs. They typically cover 80% of healthcare costs, with the remaining 20% being the responsibility of the insured. Platinum plans have the highest premiums but the lowest out-of-pocket costs. They typically cover 90% of healthcare costs, with the remaining 10% being the responsibility of the insured. When choosing a coverage level, consider your healthcare utilization and your ability to pay out-of-pocket costs. If you anticipate needing frequent medical care, a Gold or Platinum plan may be the most cost-effective option in the long run. If you're healthy and don't anticipate needing much medical care, a Bronze or Silver plan may be a better choice. Beyond the monthly premium, it's important to understand other cost-sharing mechanisms in health insurance plans. These include deductibles, copays, and coinsurance, which determine how much you'll pay out-of-pocket for healthcare services. The deductible is the amount of money you pay out-of-pocket for healthcare services before your insurance coverage kicks in. For example, if your plan has a $2,000 deductible, you'll need to pay $2,000 for covered services before your insurance starts paying its share. Plans with lower premiums typically have higher deductibles, while plans with higher premiums have lower deductibles. When choosing a plan, consider your ability to pay a large deductible if you need medical care. Some services, such as preventive care, may be covered without requiring you to meet your deductible. Check your plan's details to understand which services are covered before you reach your deductible. It's important to note that family deductibles may differ from individual deductibles. A family deductible is the total amount that the family must pay out-of-pocket before the insurance starts paying its share for the entire family. Choosing the right deductible depends on your individual circumstances and risk tolerance. If you're healthy and don't anticipate needing much medical care, a higher deductible may be a good option. If you have chronic conditions or anticipate needing frequent medical care, a lower deductible may be a better choice. A copay is a fixed fee you pay for specific healthcare services, such as doctor visits or prescription drugs. For example, you might pay a $20 copay for a visit to your primary care physician or a $10 copay for a generic prescription. Copays typically don't count towards your deductible. You pay the copay at the time of service, regardless of whether you've met your deductible. Copays can vary depending on the type of service and the plan you have. Specialist visits and emergency room visits often have higher copays than primary care visits. Some plans may have different copays for in-network and out-of-network providers. It's generally less expensive to see providers within your plan's network. When comparing plans, pay attention to the copays for the services you're likely to use. This can help you estimate your out-of-pocket costs. Coinsurance is the percentage of healthcare costs that you pay after you've met your deductible. For example, if your plan has 20% coinsurance, you'll pay 20% of the cost of covered services, and your insurance will pay the remaining 80%. Coinsurance typically applies after you've met your deductible. Once you've met your deductible, you'll start paying coinsurance until you reach your out-of-pocket maximum. Plans with lower premiums typically have higher coinsurance, while plans with higher premiums have lower coinsurance. This is another way that insurers share the cost of healthcare with their members. Coinsurance can vary depending on the type of service and the plan you have. Some services may have different coinsurance rates than others. Understanding coinsurance is crucial for estimating your out-of-pocket costs for healthcare services. It's important to factor this into your decision when choosing a health insurance plan. The out-of-pocket maximum is the most you'll pay for covered healthcare services in a given year. This includes your deductible, copays, and coinsurance. Once you reach your out-of-pocket maximum, your insurance will pay 100% of the cost of covered services for the rest of the year. This provides a financial safety net in case you experience a major illness or injury. Plans with lower premiums typically have higher out-of-pocket maximums, while plans with higher premiums have lower out-of-pocket maximums. This is an important factor to consider when choosing a plan. The out-of-pocket maximum doesn't include your monthly premium. It only applies to the costs of healthcare services. When comparing plans, pay attention to the out-of-pocket maximum. This will help you understand your potential financial exposure in the event of a major health event. The Affordable Care Act (ACA) provides subsidies and tax credits to help eligible individuals and families afford health insurance. These financial assistance programs can significantly reduce your monthly premiums and out-of-pocket costs. Premium tax credits are designed to lower your monthly health insurance premiums. They are available to individuals and families who purchase coverage through the ACA marketplace and meet certain income requirements. The amount of the premium tax credit is based on your household income and the cost of the benchmark plan (the second-lowest-cost Silver plan in your area). The credit is calculated to ensure that you don't pay more than a certain percentage of your income for health insurance. You can choose to receive the premium tax credit in advance, which will lower your monthly payments. Alternatively, you can claim the credit when you file your taxes at the end of the year. To be eligible for a premium tax credit, you must meet certain requirements, including: If you think you may be eligible for a premium tax credit, it's important to apply through the ACA marketplace. The application process will determine your eligibility and the amount of the credit you're entitled to. Cost-sharing reductions (CSRs) are designed to lower your out-of-pocket expenses, such as deductibles, copays, and coinsurance. They are available to individuals and families who purchase a Silver plan through the ACA marketplace and meet certain income requirements. CSRs reduce the amount you pay out-of-pocket for healthcare services. The level of reduction depends on your income. Individuals with lower incomes receive greater reductions. CSRs are only available with Silver plans. If you're eligible for CSRs, a Silver plan may be the most cost-effective option, even if a Bronze plan has a lower premium. To be eligible for CSRs, you must meet certain requirements, including: If you think you may be eligible for CSRs, it's important to apply through the ACA marketplace. The application process will determine your eligibility and the level of reduction you're entitled to. Medicaid and the Children's Health Insurance Program (CHIP) are government-funded programs that provide health coverage to low-income individuals and families. Medicaid provides coverage to eligible adults, children, pregnant women, seniors, and people with disabilities. Eligibility requirements vary by state. CHIP provides coverage to children in families who earn too much to qualify for Medicaid but cannot afford private health insurance. Eligibility requirements also vary by state. Medicaid and CHIP offer comprehensive health coverage, including doctor visits, hospital care, prescription drugs, and mental health services. If you think you may be eligible for Medicaid or CHIP, it's important to contact your state's Medicaid or CHIP agency. They can provide you with information about eligibility requirements and how to apply. Finding affordable health insurance requires careful planning and research. By understanding your options and utilizing available resources, you can find a plan that meets your needs and fits your budget. One of the most effective strategies for finding affordable health insurance is to shop around and compare quotes from multiple insurers. Don't settle for the first quote you receive. Use online tools and resources to compare plans and prices. The ACA marketplace allows you to compare plans offered in your state. You can also get quotes directly from insurance companies. When comparing quotes, pay attention to the monthly premium, deductible, copays, coinsurance, and out-of-pocket maximum. Consider your individual healthcare needs and your ability to pay out-of-pocket costs. Be sure to compare plans with similar coverage levels and benefits. This will help you make an informed decision. Shopping around and comparing quotes can save you a significant amount of money on your health insurance premiums. A high-deductible health plan (HDHP) may be a good option if you're looking for a lower monthly premium. HDHPs have lower premiums but higher deductibles. HDHPs are often paired with a Health Savings Account (HSA), which allows you to save money tax-free for healthcare expenses. You can use the money in your HSA to pay for your deductible, copays, and other healthcare costs. HDHPs may be a good option if you're healthy and don't anticipate needing much medical care. However, if you have chronic conditions or anticipate needing frequent medical care, an HDHP may not be the best choice. Before choosing an HDHP, consider your ability to pay a large deductible if you need medical care. HDHPs can be a cost-effective option for some individuals and families. However, it's important to weigh the pros and cons before making a decision. Increasing your deductible is another way to lower your monthly health insurance premium. Plans with higher deductibles typically have lower premiums. Before increasing your deductible, consider your ability to pay a higher deductible if you need medical care. Make sure you have enough savings to cover the higher deductible. Increasing your deductible can save you money on your monthly premiums, but it also increases your out-of-pocket costs if you need medical care. This strategy is best suited for individuals who are healthy and don't anticipate needing much medical care. Carefully consider your risk tolerance and financial situation before increasing your deductible. Catastrophic health plans are designed to protect you from catastrophic medical expenses. They have very high deductibles and low monthly premiums. Catastrophic plans are only available to individuals under age 30 or those who qualify for a hardship exemption. Catastrophic plans cover essential health benefits, but you'll need to pay all of your healthcare costs out-of-pocket until you meet the high deductible. Catastrophic plans may be a good option if you're young and healthy and primarily concerned about protecting yourself from a major medical event. Before choosing a catastrophic plan, carefully consider your ability to pay the high deductible if you need medical care. Many health insurance plans cover preventative care services without requiring you to meet your deductible or pay a copay. Taking advantage of these services can help you stay healthy and avoid more costly medical treatments in the future. Preventative care services include annual physicals, vaccinations, screenings, and other services designed to detect and prevent health problems. By utilizing preventative care services, you can reduce your risk of developing chronic conditions and requiring expensive medical treatments. Check your plan's details to understand which preventative care services are covered without cost-sharing. Taking care of your health through preventative care can save you money on healthcare costs in the long run. Now that we've covered the factors that influence premiums and strategies for finding affordable coverage, let's dive into some actual cost figures. It's important to remember that these are just averages and your individual costs may vary significantly. The national average health insurance premium varies depending on factors like age, plan type, and coverage level. However, it's useful to have a general idea of what to expect. According to recent data, the average monthly premium for an individual health insurance plan purchased through the ACA marketplace is around $500-$600. However, this figure can vary widely depending on the factors mentioned earlier. Family premiums are significantly higher, often exceeding $1,500 per month. This reflects the increased cost of covering multiple individuals. Keep in mind that these are just averages. Your actual premium may be higher or lower depending on your specific circumstances. It's always best to get personalized quotes from multiple insurers to get an accurate estimate of your health insurance costs. As we discussed earlier, age is a significant factor in determining health insurance premiums. Let's take a look at how premiums typically vary by age group. Young adults (ages 18-24) generally pay the lowest premiums, often around $300-$400 per month. This is because they are statistically less likely to require extensive medical treatment. Individuals in their 30s and 40s typically pay premiums in the range of $400-$600 per month. This reflects the increasing risk of health problems as individuals age. Individuals in their 50s and 60s often pay premiums exceeding $700 per month. This is due to the higher likelihood of developing age-related health conditions. These are just general guidelines. Your actual premium may vary depending on other factors, such as your location and health status. It's important to note that the ACA limits the amount by which insurers can increase premiums based on age. However, age remains a significant factor in determining health insurance costs. The type of health insurance plan you choose will also affect your monthly premium. Let's compare the average premiums for different plan types. HMO plans typically have the lowest premiums, often in the range of $400-$500 per month. This is because HMOs require you to choose a primary care physician and coordinate your care through them. PPO plans have slightly higher premiums, often in the range of $500-$600 per month. This is because PPOs offer more flexibility and allow you to see any doctor or specialist without a referral. EPO plans have premiums that are similar to PPO plans, often in the range of $500-$600 per month. EPOs offer less flexibility than PPOs, as you're generally only covered if you see providers within the plan's network. HDHPs have lower premiums than other plan types, often in the range of $300-$400 per month. However, they also have higher deductibles. These are just general guidelines. Your actual premium may vary depending on other factors, such as your location and health status. The coverage level you choose (Bronze, Silver, Gold, or Platinum) will also impact your monthly premium. Let's compare the average premiums for different coverage levels. Bronze plans have the lowest premiums, often in the range of $300-$400 per month. However, they also have the highest out-of-pocket costs. Silver plans have moderate premiums, often in the range of $400-$500 per month. They also have moderate out-of-pocket costs. Gold plans have higher premiums, often in the range of $500-$600 per month. They also have lower out-of-pocket costs. Platinum plans have the highest premiums, often exceeding $600 per month. They also have the lowest out-of-pocket costs. The best coverage level for you depends on your healthcare needs and your ability to pay out-of-pocket costs. Health insurance costs can vary significantly from one state to another. Let's take a look at some examples of regional variations. States with a higher cost of living and a greater utilization of medical services tend to have higher premiums. These states include California, New York, and Massachusetts. States with a lower cost of living and a lower utilization of medical services tend to have lower premiums. These states include Utah, Idaho, and North Dakota. State regulations also play a role in determining premiums. Some states have implemented regulations that limit the amount by which insurers can increase premiums, while others have more lenient regulations. To get an accurate estimate of your health insurance costs, it's essential to compare quotes from insurers that operate in your specific state. Choosing the right health insurance plan is a complex decision that requires careful consideration of your individual needs and financial situation. By understanding the factors that influence premiums, the different types of plans available, and the resources available to help you afford coverage, you can make an informed decision that protects your health and your wallet. When considering your **Health Insurance Cost Per Month: What to Expect?**, be sure to weight all options.

Before you start shopping for health insurance, take some time to assess your healthcare needs. Consider factors like your age, health status, family history, and lifestyle. Do you have any chronic conditions that require regular medical care? Do you take any prescription medications? Do you anticipate needing frequent doctor visits or hospitalizations? If you have significant healthcare needs, you may want to choose a plan with lower deductibles and copays, even if it means paying a higher monthly premium. If you're healthy and don't anticipate needing much medical care, you may be able to save money by choosing a plan with higher deductibles and copays. It's important to be realistic about your healthcare needs when choosing a plan. Don't underestimate the potential cost of medical care. Health Insurance Cost Per Month: What to Expect?, It's also important to set a budget for your health insurance. Determine how much you can afford to spend each month on premiums and out-of-pocket costs. Consider your other financial obligations, such as rent, mortgage payments, car payments, and student loans. Don't overextend yourself by choosing a plan that you can't afford. It's better to choose a more affordable plan, even if it means sacrificing some coverage. Remember to factor in the potential cost of out-of-pocket expenses, such as deductibles, copays, and coinsurance. Sticking to your budget will help you avoid financial hardship in the future. Before you enroll in a health insurance plan, be sure to read the fine print. Pay attention to the plan's details, including the deductible, copays, coinsurance, out-of-pocket maximum, and covered services. Make sure you understand the plan's network of providers. Are your doctors and hospitals in the plan's network? Read the plan's summary of benefits and coverage (SBC). This document provides a clear and concise overview of the plan's benefits and costs. If you have any questions about the plan, don't hesitate to contact the insurance company or a licensed insurance agent. Understanding the plan's details will help you avoid surprises and make informed decisions about your healthcare. If you're feeling overwhelmed by the process of choosing a health insurance plan, consider seeking professional advice from a licensed insurance agent. An agent can help you understand your options, compare plans, and choose the coverage that's right for you. A licensed agent can also help you determine if you're eligible for government subsidies or tax credits. Agents are typically paid a commission by the insurance company, so their services are usually free to you. When choosing an agent, make sure they are licensed and experienced. Ask them about their qualifications and their experience with health insurance. Working with a licensed agent can make the process of choosing health insurance much easier and less stressful. Your healthcare needs and financial situation may change over time. It's important to review your health insurance coverage annually to ensure that it still meets your needs. Did you have any major medical expenses in the past year? Did you experience any changes in your health status? Did your income change? If your needs have changed, you may need to adjust your coverage. You may want to increase your coverage if you anticipate needing more medical care in the future. You can make changes to your health insurance coverage during the annual open enrollment period. Reviewing your coverage annually will help you ensure that you have the right coverage at the right price. Understanding **Health Insurance Cost Per Month: What to Expect?** is crucial for making informed decisions about your healthcare. By considering the various factors that influence premiums, exploring different plan types, and utilizing available resources, you can find coverage that meets your needs and fits your budget. Remember to shop around, compare quotes, and seek professional advice when needed.

The world of health insurance can seem daunting, but with the right knowledge and resources, you can navigate it successfully. By taking the time to understand your options and make informed decisions, you can protect your health and your financial well-being. We hope this guide has provided you with valuable insights into the complexities of health insurance costs. We encourage you to explore other articles on our website for more information on related topics. We strive to provide you with the knowledge and resources you need to make informed decisions about your healthcare. Stay informed, stay healthy, and stay proactive in managing your healthcare costs. Check out our other articles on topics such as "Understanding Your Health Insurance Deductible," "Navigating the Affordable Care Act Marketplace," and "Tips for Saving Money on Prescription Drugs."Factors Influencing Your Monthly Premium

Age: A Key Determinant

Location: Where You Live Matters

Health Status: Pre-Existing Conditions and More

Plan Type: HMO, PPO, and More

Coverage Level: Bronze, Silver, Gold, and Platinum

Understanding Deductibles, Copays, and Coinsurance

Deductibles: Your Out-of-Pocket Threshold

Copays: Fixed Fees for Services

Coinsurance: Sharing the Costs

Out-of-Pocket Maximum: Your Financial Safety Net

Government Subsidies and Tax Credits: Reducing Your Costs

Premium Tax Credits: Lowering Your Monthly Payments

Cost-Sharing Reductions: Reducing Your Out-of-Pocket Expenses

Medicaid and CHIP: Coverage for Low-Income Individuals and Families

Strategies for Finding Affordable Health Insurance

Shop Around and Compare Quotes

Consider a High-Deductible Health Plan (HDHP)

Increase Your Deductible

Explore Catastrophic Plans

Utilize Preventative Care Services

Health Insurance Cost Per Month: What to Expect? The Numbers

National Average Premiums: A Snapshot

Premiums by Age Group: The Age Factor in Action

Premiums by Plan Type: HMO vs. PPO vs. EPO

The Impact of Coverage Level: Bronze, Silver, Gold, and Platinum

Understanding Regional Variations: State by State Differences

Making Informed Decisions About Your Health Insurance

Assess Your Healthcare Needs: What Do You Really Need?

Set a Budget: How Much Can You Afford?

Read the Fine Print: Understanding Plan Details

Seek Professional Advice: Talk to a Licensed Agent

Review Your Coverage Annually: Adjust as Needed

Conclusion

- National Average: Around $500 - $600 per month for individual plans.

- Young Adults (18-24): Typically $300 - $400 per month.

- Individuals (30s-40s): Roughly $400 - $600 per month.

- Older Individuals (50s-60s): Often exceed $700 per month.

- HMO Plans: Generally $400 - $500 per month.

- PPO Plans: Usually $500 - $600 per month.

- Bronze Plans: Commonly $300 - $400 per month.